![]()

Written by Anup V Naick

Games and Technology Editor | Reviewed for accuracy | Updated July 13, 2026 | 8 min read

Friendly Fraud Chargebacks: What They Are and How to Fight Them

Quick answer

Friendly fraud chargebacks happen when a customer disputes a legitimate charge with their bank instead of contacting the merchant, often by claiming the purchase was unauthorised, the item never arrived, or they do not recognise the transaction. Unlike criminal fraud, no stolen card is involved. Merchants can fight these disputes by submitting compelling evidence such as delivery confirmation, IP logs, signed receipts, and communication history within the card network’s response window, usually 20 to 45 days.

If a charge on your statement suddenly gets disputed even though you or your customer actually made the purchase, you are looking at friendly fraud. It is one of the fastest growing categories of payment disputes worldwide, and it costs merchants far more than the transaction amount once fees and lost goods are added up.

What is a friendly fraud chargeback

A friendly fraud chargeback is a payment dispute filed by a genuine cardholder against a transaction they personally authorised. The term “friendly” is misleading. There is nothing friendly about the outcome for a merchant, who typically loses the sale amount, the shipped goods or delivered service, and a chargeback processing fee, all at once.

Friendly fraud differs from criminal card fraud in one key way. In criminal fraud, someone else uses a stolen card without the owner’s knowledge. In friendly fraud, the cardholder made the purchase but disputes it anyway, sometimes by mistake, sometimes out of frustration with a merchant’s return policy, and sometimes deliberately to get a product for free.

Common reasons customers file friendly fraud disputes

- Subscription confusion: The customer forgot about a recurring charge or did not recognise the billing descriptor on their statement.

- Family sharing: A spouse, partner, or family member made the purchase and the cardholder was not aware of it.

- Impatience with delivery: The order is delayed and the customer disputes it before contacting the merchant.

- Buyer’s remorse: The customer changed their mind after purchase and finds a dispute easier than a return.

- Deliberate abuse: A small share of disputes are intentional attempts to keep goods while getting a refund, sometimes called cyber shoplifting.

Friendly fraud versus criminal fraud versus merchant error

Not every chargeback is friendly fraud. Banks and payment processors generally group disputes into three buckets, and knowing which one applies changes how a business should respond.

| Dispute type | Who acted | Typical outcome |

|---|---|---|

| Friendly fraud | Genuine cardholder | Reversible with strong evidence |

| Criminal fraud | Unauthorised third party | Usually ruled for the cardholder |

| Merchant error | Business made a mistake | Usually ruled for the cardholder |

| Item not received | Depends on shipping proof | Depends on tracking evidence |

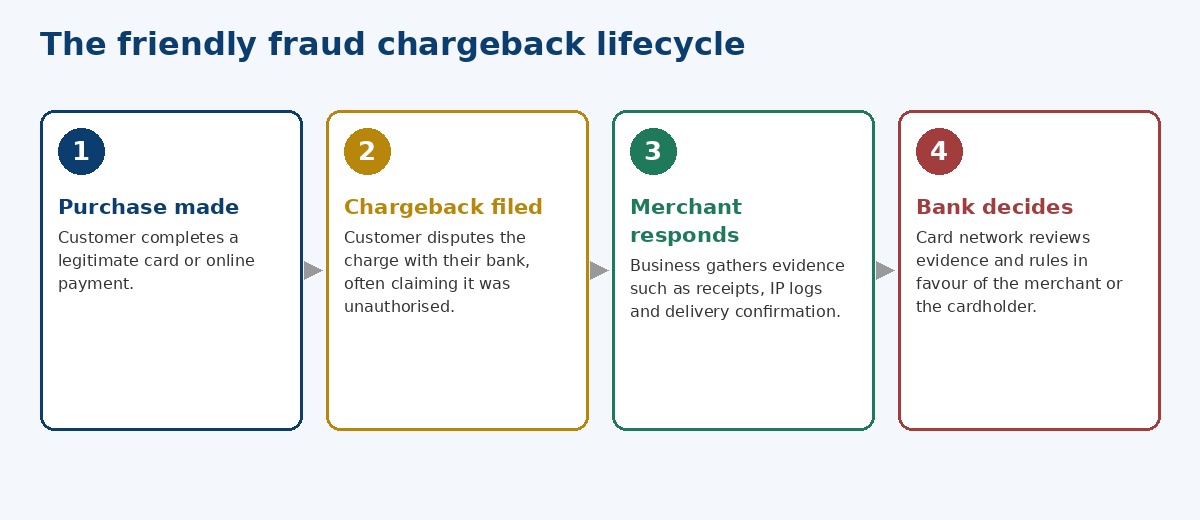

The chargeback dispute lifecycle

Every chargeback moves through the same four broad stages, regardless of the card network involved.

Evidence that helps merchants win a dispute

- Delivery confirmation: Signed proof of delivery or a tracking number showing the package reached the billing or shipping address.

- IP address and device data: Matches the cardholder’s usual location or device fingerprint.

- Order and communication history: Emails, chat logs, or support tickets showing the customer engaged with the order.

- Terms of service acceptance: Timestamped proof the customer agreed to a subscription or refund policy.

- AVS and CVV match results: Address verification and card security code confirmation from the original transaction.

How merchants can reduce friendly fraud

Prevention is cheaper than fighting disputes after they happen. According to the Federal Reserve’s payments research, card not present transactions carry a materially higher dispute rate than in person purchases, which makes proactive controls especially important for online sellers.

- Use a clear, recognisable billing descriptor that matches your brand name.

- Send order and shipping confirmation emails immediately, with tracking links.

- Offer an easy, visible refund and cancellation process so customers contact you first.

- Require CVV and address verification on every card not present transaction.

- Flag repeat disputers and apply extra verification on future orders.

- Keep subscription billing reminders active before every renewal charge.

Tools that support dispute management

Payment processors and card networks now offer real time alert services that notify a merchant before a dispute is officially filed, giving a short window to issue a refund and avoid a formal chargeback altogether. The Consumer Financial Protection Bureau also outlines the cardholder side of this process, which is useful reading for merchants who want to understand what a genuine dispute claim looks like from the customer’s perspective.

If you are comparing the cost of chargebacks against your margins, our financial calculators hub includes a simple margin and fee calculator that can help estimate the real cost of a dispute once processing fees are included. For a wider view of how payment disruptions get tracked, see our outage and service status tracker, which covers banking and payment platform incidents as they happen.

Frequently asked questions

Is friendly fraud a crime

It can be, if the cardholder knowingly disputes a charge to avoid paying for something they received. In practice it is rarely prosecuted because intent is hard to prove, so most cases are resolved through the card network’s dispute process rather than the courts.

How long do merchants have to respond to a chargeback

Response windows typically range from 20 to 45 days depending on the card network and region. Missing the deadline usually means an automatic loss for the merchant, so fast evidence collection matters.

Can a customer be banned for repeated friendly fraud

Yes. Many merchants track repeat disputers and refuse future orders, and some payment processors maintain shared negative lists that flag customers with a pattern of unjustified disputes.

TLDR: Friendly fraud chargebacks in brief

- Friendly fraud is a dispute filed by the genuine cardholder, not a stolen card.

- Common triggers are subscription confusion, family purchases, and delayed delivery.

- Merchants can fight disputes with delivery proof, IP data, and communication logs.

- Response windows are usually 20 to 45 days, so evidence should be gathered fast.

- Clear billing descriptors and visible refund policies prevent most disputes upfront.

About the Author

Anup V Naick is the founder of Wings Infotech and writes on financial, regulatory, and public interest topics. He holds a Mechanical Engineering degree from Manipal Institute of Technology and an MBA from TKM Institute of Management. Editorial claims in this article are cross checked against card network and regulatory guidance before publishing.

📧 contact@seminarsonly.com | facebook.com/seminarsonly | twitter.com/seminarsonly

🌐 seminarsonly.com

Pingback: Google: "Some of Your Saved Passwords Were Found Online" — What to Do Immediately [2026] - Seminarsonly.com