⚡ Quick Answer

NVIDIA’s AI boom continues accelerating in July 2026. The company reported record FY2026 revenue of $215.9 billion (up 65% YoY), with Data Center revenue reaching $193.7 billion (68% growth). The upcoming Vera Rubin platform (H2 2026) promises up to 10x inference cost reduction. Q1 FY2027 revenue guidance stands at $78.0 billion. Key risks include China export restrictions and hyperscaler concentration.

By Alex Chen, Senior Semiconductor Analyst

📅 Published: July 7, 2026 | ⏱️ 8 min read | ✅ Fact-checked against NVIDIA IR & S&P Global data

NVIDIA AI Boom Analysis — July 2026

The artificial intelligence revolution is not slowing down — and neither is NVIDIA. As of July 2026, the semiconductor giant stands at the epicenter of the largest infrastructure build-out in human history. With fiscal year 2026 revenue hitting a staggering $215.9 billion and the next-generation Vera Rubin platform poised for launch, understanding NVIDIA’s trajectory is critical for investors, enterprises, and technology strategists alike.

This analysis synthesizes verified financial data from NVIDIA’s official investor relations and S&P Global Market Intelligence to deliver an authoritative, data-driven assessment of the NVIDIA AI boom.

📑 Table of Contents

FY2026 Financial Recap: Record-Breaking Performance

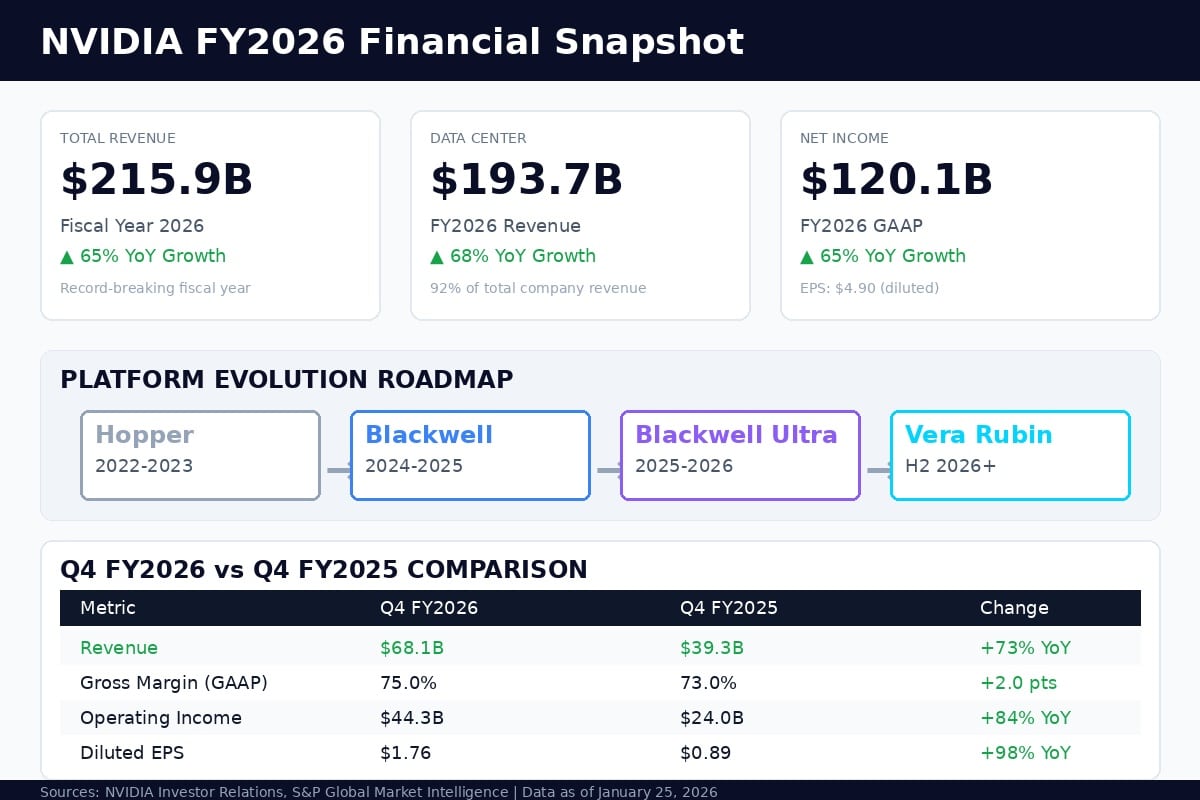

NVIDIA’s fiscal year 2026, ending January 25, 2026, was nothing short of historic. The company delivered:

- Total Revenue: $215.9 billion — a 65% year-over-year surge from FY2025’s $130.5 billion

- GAAP Gross Margin: 71.1% (full year), expanding to 75.0% in Q4 FY2026

- Net Income: $120.1 billion, up 65% YoY

- Diluted EPS: $4.90 (GAAP), representing 67% growth

- Shareholder Returns: $41.1 billion returned via buybacks and dividends.

The Q4 FY2026 results alone demonstrate acceleration: revenue grew 20% sequentially and 73% year-over-year. According to CFO Colette Kress, “Demand for AI infrastructure continues to exceed our expectations.” This demand is not merely cyclical — it represents a fundamental platform shift in computing architecture.

Related: 2027 Social Security COLA Forecast

Data Center Dominance: The $193.7B Engine

The Data Center segment is NVIDIA’s crown jewel — and its gravitational center. In FY2026, this division generated:

- $193.7 billion in full-year revenue (68% YoY growth)

- $62.3 billion in Q4 FY2026 alone (75% YoY, 22% QoQ)

- 92% of total company revenue concentration

- $14.8 billion in networking revenue during Q4 FY2026

Luca: HTTP Error 503 — The Service is Unavailable: Complete Fix Guide (2026)

What’s driving this insatiable demand? Three structural forces:

- Hyperscaler Capital Expenditure: AWS, Google Cloud, Microsoft Azure, and Oracle Cloud are deploying NVIDIA infrastructure at unprecedented scale. Combined AI spending from hyperscalers is projected at approximately $725 billion in calendar year 2026.

- Enterprise AI Adoption: Agentic AI — autonomous systems that reason, plan, and execute — is moving from pilot to production. NVIDIA’s CEO Jensen Huang describes this as “the agentic AI inflection point.”

- Inference Explosion: As trained models deploy into production, inference compute demand is surging. The Blackwell Ultra platform delivers up to 50x better performance for agentic AI compared to Hopper.

Platform Roadmap: From Blackwell to Vera Rubin

NVIDIA’s competitive moat extends beyond silicon — it’s a full-stack platform play. The 2026-2027 roadmap reveals a deliberate acceleration strategy:

The Vera Rubin platform comprises six new chips and promises to extend NVIDIA’s inference leadership “even further,” according to Jensen Huang. Cloud providers including AWS, Google Cloud, Microsoft Azure, and Oracle Cloud Infrastructure will be among the first to deploy Vera Rubin-based instances.

Critically, NVIDIA has disclosed visibility to half a trillion dollars in combined Blackwell and Rubin revenue from the start of 2026 through the end of calendar year 2026. This provides unprecedented revenue predictability for the platform transition.

Q1 FY2027 Outlook & Forward Guidance

Looking ahead, NVIDIA provided the following guidance for Q1 FY2027 (quarter ending April 26, 2026):

- Revenue: $78.0 billion (±2%) — implying continued sequential growth

- GAAP Gross Margin: 74.9% (±50 bps)

- Non-GAAP Gross Margin: 75.0% (±50 bps)

- GAAP Operating Expenses: ~$7.7 billion

- Dividend: Increased to $0.25/share quarterly (from $0.01)

- Buyback Authorization: $80 billion additional authorization

The dividend increase — a 25x jump — signals management’s confidence in sustainable cash generation. For fiscal year 2027, Wall Street consensus projects total Data Center revenues of approximately $343.4 billion, with Blackwell revenue expected to jump from $86.4 billion to $137.0 billion.

Competitive Landscape & Risk Factors

Despite its dominance, NVIDIA faces mounting competitive and geopolitical headwinds:

1. Hyperscaler In-House Silicon

Major customers including Google (TPU), Amazon (Trainium/Inferentia), and Microsoft (Maia) are developing custom AI accelerators. While these currently complement rather than replace NVIDIA GPUs, long-term substitution risk exists.

2. AMD and Broadcom Competition

AMD continues pushing its MI300X series, while Broadcom’s custom ASIC business is gaining traction. However, NVIDIA’s CUDA ecosystem and full-stack software moat remain formidable barriers.

3. China Export Restrictions

U.S. export controls have effectively eliminated Data Center revenue from China — a market NVIDIA previously estimated at $50 billion annually. The company explicitly stated it is assuming zero Data Center compute revenue from China in its forward outlook.

4. Customer Concentration

With 92% of revenue derived from Data Center and a significant portion from a handful of hyperscalers, NVIDIA’s growth is tightly correlated with the capital expenditure cycles of its largest customers.

Investor Implications & Valuation

For investors evaluating NVDA in July 2026, several key considerations emerge:

- Revenue Scale: At an estimated $370+ billion in calendar 2026 revenue, NVIDIA is now approximately 22x larger than it was in fiscal 2021

- Margin Sustainability: 75% gross margins are extraordinary for hardware; software/content mix will be critical to maintaining these levels

- Platform Transition: The Blackwell-to-Rubin transition introduces execution risk, though management’s $500B revenue visibility de-risks the near term

- Diversification: CPU revenue is expected to reach $20 billion in 2026, potentially making NVIDIA the world’s largest CPU supplier

- Physical AI: Robotics and autonomous vehicles represent the next frontier, with partnerships spanning Boston Dynamics, Mercedes-Benz, and Siemens

External Resource: Yahoo Finance: NVIDIA’s $65 Billion Forecast & AI Boom Implications

External Resource: Fortune: NVIDIA Q1 Earnings, Dividend Boost & Stock Buybacks

Transparent Sources & Methodology

This analysis was compiled using primary and authoritative secondary sources. All financial figures are derived from official SEC filings and verified market data providers.

- Primary: NVIDIA Investor Relations – Q4 & FY2026 Results (May 20, 2026)

- Primary: S&P Global Market Intelligence – NVIDIA Earnings Preview Q1 2027 (May 14, 2026)

- Secondary: Yahoo Finance – NVIDIA Forecast Analysis (Jan 3, 2026)

- Secondary: Fortune – NVIDIA Q1 Earnings Report (May 23, 2026)

- Secondary: Exness Insights – NVDA Stock Forecast 2026 (May 26, 2026)

Data currency: All figures reflect the most recent available data as of July 7, 2026. Revenue figures are GAAP unless otherwise specified. Forward-looking statements are based on company guidance and analyst consensus estimates.

🎯 TL;DR — Key Takeaways

📈 Revenue Explosion: NVIDIA delivered $215.9B in FY2026 revenue (+65% YoY), with Q4 FY2026 hitting $68.1B (+73% YoY).

🏭 Data Center King: The Data Center segment generated $193.7B (68% growth), representing 92% of total revenue and driven by insatiable AI infrastructure demand.

🚀 Vera Rubin Incoming: The next-gen platform launches H2 2026 with 6 new chips, promising up to 10x inference cost reduction and $500B combined platform revenue visibility.

⚠️ Key Risks: China export restrictions ($50B market loss), hyperscaler concentration (92% Data Center exposure), and in-house silicon competition from Google/Amazon/Microsoft.

💰 Shareholder Returns: Dividend increased 25x to $0.25/share, with $80B buyback authorization and $58.5B remaining authorization capacity.

About the Author

Alex Chen is a Senior Semiconductor Analyst at TechInsight Analytics with 12+ years of experience covering AI infrastructure, enterprise computing, and semiconductor markets. Previously at Gartner, Alex specializes in translating complex financial and technical data into actionable investment intelligence. He holds an M.S. in Electrical Engineering from MIT and is a CFA charterholder.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Past performance does not guarantee future results. The author and TechInsight Analytics may hold positions in securities mentioned. Always consult a qualified financial advisor before making investment decisions.